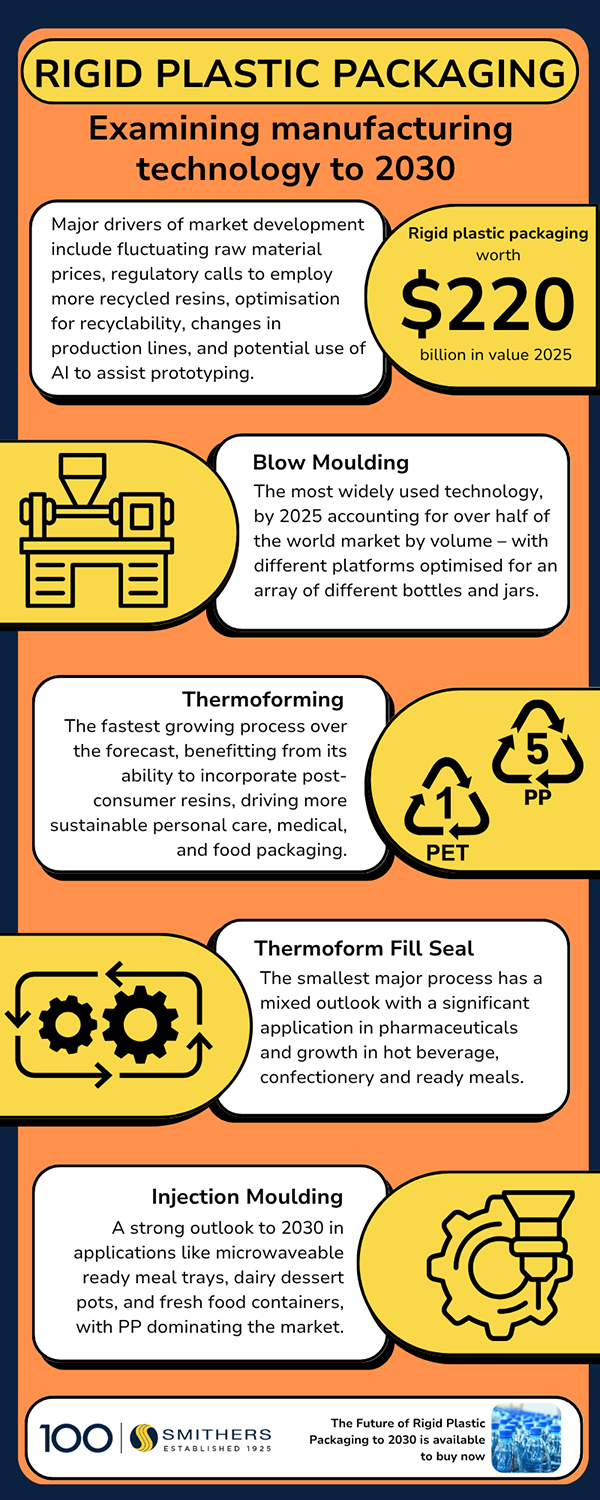

Consuming 67.9 million tonnes of polymers and worth a projected $220.2 billion in 2025, rigid plastic packaging represents a lucrative sector of the global packaging market.

Manufacturing technology outlook

Multiple factors are acting on rigid plastic converters: fluctuating raw material prices, regulatory calls for more recycled resins, the optimisation of designs for recyclability, adapting to changes in production lines, and the potential of AI-assist prototyping.

Detailed market forecasting in the latest Smithers market report –

The Future of Rigid Plastic Packaging to 2030 examines how these will interact across the next five years.

Global consumption is forecast to reach 80.8 million tonnes in 2030, with value at constant pricing reaching $262.7 billion. This will support further innovation in the four principal rigid plastic manufacturing technologies.

Blow moulding

Blow moulding is the most widely used technology – accounting for 57.6% of the world market by volume in 2025 – with different platforms optimised for an array for different bottles and jars.

Blow moulded polyethylene terephthalate (PET) has grown rapidly over the last decade, but demand is now slowing as applications like bottled water and carbonated soft drinks reach a saturation point in developed markets. Smithers forecasts a more positive outlook for blow moulded polypropylene (PP) as processing technologies improve, and better clarified PP bottle grades become available.

Thermoforming

Thermoforming is the second major process, benefitting from the greater availability of roll-fed configurations and in-factory sheet extrusion equipment. It will be the fastest growing production process across 2025-2030, supporting increased consumption of PP in rigid plastic packaging.

Thermoforming is well suited for many food packaging formats – butter, margarine, ice cream, yogurt tubs and pots; fresh protein and ready meal trays; sandwich packs; and vending machine cups. There are ongoing developments in 3D modelling and virtual prototyping software, which are being enhanced further by new artificial intelligence (AI) algorithms.

The segment will also benefit from the capacity to incorporate post-consumer resins (PCR) in thermoforming processes.

Injection moulding

Injection moulding is a rapid manufacturing process for identical closures, crates, pails or food containers, where customisation is mostly achieved via decoration. Overall Smithers forecasts a drop in market share for injection moulding, although the outlook to 2030 is stronger in some applications – such as microwaveable ready meal trays, dairy dessert pots, and fresh food containers.

PP dominates the market and is still gaining share from the second main polymer, PE. Polystyrene (PS) has lost ground to PP for cost reasons, and is now largely confined to dairy dessert packs.

Thermoform-fill-seal

Thermoform-fill-seal, the smallest major process, has a mixed outlook. Demand from dairy goods has matured, but is accelerating for hot beverage, baked goods, confectionery, and ready meal packaging. In pharmaceuticals, blister packs are a major application, but again more companies are bringing this process in-house, with work also underway to replace PVC with easier to recycle commodity plastics.